The Big Question: Should You Buy a Home or Rent One?

“Home is not a place; it’s a feeling.” (Cecelia Ahern)

Deciding whether to buy or rent your home may be one of the most important financial decisions you’ll ever make. Ultimately, the choice comes down to a combination of financial variables and personal factors, which, as we know, fluctuate unpredictably.

Rands and cents

Let’s start by comparing the costs of renting and buying a home.

If you rent a home, the costs include the following:

- The basic rental amount and an upfront deposit, which could be two or three times the monthly rent amount.

- Water and electricity are usually additional costs, but levies and taxes may also need to be paid, depending on the rental agreement.

If you buy a home, the costs include:

- The mortgage repayments (assuming you need a mortgage, please bear in mind that interest rates change).

- The administrative costs, including securing the mortgage and transferring attorney’s fees.

- Transfer duty (which is high in South Africa),

- Property taxes and levies, and maintenance (more about this below)

The hidden costs of ownership

One often overlooked cost when deciding to buy is the cost of maintenance. The 1% rule advises setting aside at least 1% of the home’s value every year for upkeep. This is a significant financial commitment. Over many years, you may need to set aside up to 4% for major expenses such as replacing the roof.

Another hidden cost of homeownership is opportunity cost. By investing in a house, you’re forgoing the potential returns from investing in equity, which will most likely be higher than the long-term return on residential property.

If you prefer the stock market to homeownership, it’s crucial to be diligent and invest a similar amount in long-term investments for retirement (this is one case where debit orders are your friend) as you would for a mortgage. Unlike your rental payment, which you can’t renege on, spending on unnecessary items is easy when you don’t have a mortgage, which could jeopardise your long-term financial security. Understanding this opportunity cost will help you make a cautious and informed decision.

Remember, there’s more to life than money

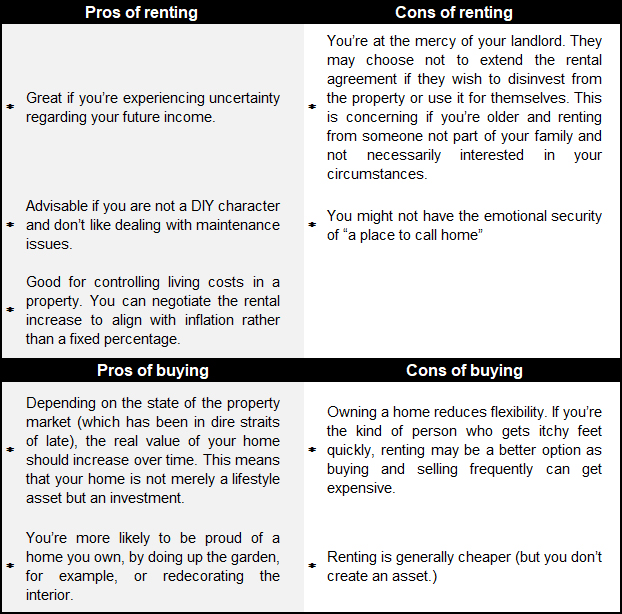

Let’s consider some of the other pros and cons of renting versus buying.

The 8.5% rule

In addition to the 1% rule for maintenance costs of ownership, another widely accepted rule of thumb is the 8.5% one!

This suggests that renting may be more cost-effective if the annual cost of owning a home (including mortgage payments, property taxes, insurance, and maintenance) exceeds 8.5% of the home’s purchase price. However, this rule is a rough estimate, and your financial circumstances, values, and goals must be considered.

Another rule of thumb

Even if you’re set on owning a home, it’s important not to buy a home that is too expensive for your means. Another rule of thumb suggests you shouldn’t spend more than 28% of your gross income on a mortgage repayment. But it’s a broad rule of thumb! The actual recommended percentage should consider your net income and average tax rate.

Crunching the numbers

We can assist you in discussing all of the above and crunching the numbers. But please bear in mind that the numbers and forecasts are subjective in that we need to assume specific factual variables, including future:

- Interest rates

- Inflation rates

- Return on residential property

- Political stability

- Return on equity

- Expected annual rental increases.

What about retirement capital?

Many of our clients believe a fully paid-up home can assist in providing for retirement. This is not necessarily true. The costs of downsizing may not release much capital, considering the costs of moving, including transfer duty and estate agent’s fees. You’ll also have to bear the costs of living in a retirement complex. Generally, life rights agreements favour the property developer rather than the retiree and their beneficiaries.

The bottom line

Ultimately, your decision should align with your priorities (including emotional priorities), lifestyle, and market expectations. We can consider factors like affordability, long-term plans, and whether you view your home primarily as an investment or a lifestyle asset.

As Cecilia Ahern said, “Home is not a place; it’s a feeling.” Like it or not, we all need a home that gives us emotional security. The fundamental issue is whether a rental property can provide a sense of ‘home’.

We’re here to assist you in your decision-making! Contact us before you decide on renting or owning a home.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© FinDotNews